1. Problem recognition, definition and evaluation

Earned value techniques (EVT) are selected consistent with the way planned work is to be performed. EVM provides PMs with early warning of inadequate performance that allows them to take necessary corrective action before the project spins out of control and is not recoverable. Hence, selecting the appropriate earned value technique is crucial to the effectiveness of earned value data for proactive program control, making program decisions and timely reporting.

2. Development of the feasible alternatives

There are numerous recognized Earned Value Techniques/Methods available to measure tasks/activities performance/progress:

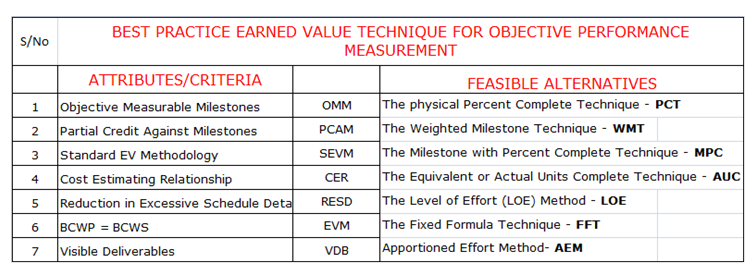

1. The physical Percent Complete Technique – requires that Control Accounts (CAM) measures or estimates the percent of actual physical progress that has been achieved on the WP, relative to the total value (BAC) of the WP. The percent complete is applied to the BAC to determine cumulative BCWP (EV).

2. The Weighted Milestone Technique – requires that the Work Package be defined in terms of interim milestones, at least one per accounting period. When each milestone is completed, 100 percent of the respective budget value is earned.

3. The Milestone with Percent Complete Technique – It requires that the Work Package be defined in terms of sequential milestones, it is especially effective when Work Packages have short duration (say less than six weeks).

4. The Equivalent or Actual Units Complete Technique - The Actual Units Complete EVM method is used for repetitive tasks using Line of Balance (LoB) scheduling, i.e. tasks involving the same work; e.g. the installation of 10” gate valves in a linear meter run of pipeline. One unit installed is actual value earned.

5. The Level of Effort (LOE) Method – This method sets incremental earned value equal to the planned (budgeted) amount and precludes (prevents) any schedule variance, i.e. BCWP = BCWS.

6. The Fixed Formula Technique provides easy handling of short-term activities, i.e. activities that span one to two accounting periods. The 0/100 and 50/50 splits are common forms of this method; 0/100 is applicable to an activity confined to a single accounting period , 50/50 is used where the activity may start in one month and end in the next accounting month. Procurement activities can be measured more accurately using this method.

7. Apportioned Effort Method - is also referred to as factored effort or factored method. It is used to calculate earned value for tasks that are related in direct proportion to a parent work package.

3. Development of the outcomes and cash flows for each alternative

4. Selection of the acceptable criteria

Earned value techniques are selected consistent with the way planned work is to be performed. The EVMS must be reviewed with the customer during the IBR, based on acceptable criteria such as; Objective measurable milestones, partial credit against milestones, standards earned methodology, mirror established cost estimating relationship. Monthly budget value is earned with the passage of time and is equal to the monthly scheduled amount (BCWP = BCWS).

5. Analysis and Comparison of the alternatives

Detailed supporting documentation is typically required during the IBR to demonstrate a clear measurement approach and strategy. Applying the physical percent complete technique is based on objective measurable milestones, which the customer prefers, and allows for partial credit against milestones. While use of subjective EVM methods such as Level of Effort (LOE), Expert Judgment and Apportioned Effort not measured objectively is always subject to challenge.

6. Selection of the preferred alternative

The Physical Percent Complete Technique requires objective measurable milestones, which the customer prefers, and allows for partial credit against milestones. This EVT can reduce excessive schedule details by representing numerous activities as internal milestones within a single work package.

7. Performance Monitoring and Post Evaluation of Results

EVM provides PMs with early warning of inadequate performance that allows them to take necessary corrective action before the project spins out of control and is not recoverable. Warning of problems is usually available to management before 15 percent of the program is complete, in time to take corrective measures to alter an unfavorable outcome.

8. References/Bibliography

1. Earned Value Management Best Practices. Guidance on three commonly asked questions. Presented by. Michael R. Nosbisch, CCC, PSP:

2. Kimberly, Meyer EVP, and Kimberly, Hunter EVP, AACE Cost Engineering Journal March/April 2013 Edition:

3. AACE International Recommended Practice Updated No. 11R-88